ARCHIVED – Canadian Energy Dynamics: Review of 2014 – Energy Market Assessment

This page has been archived on the Web

Information identified as archived is provided for reference, research or recordkeeping purposes. It is not subject to the Government of Canada Web Standards and has not been altered or updated since it was archived. Please contact us to request a format other than those available.

February 2015

Canadian Energy Dynamics: Review of 2014 - Energy Market Assessment [PDF 3595 KB]

ISSN 2292-8308

Copyright/Permission to Reproduce

Table of Contents

Photo of steam rising from the ENMAX district heating plant in downtown Calgary on a chilly day in January.

- Canadian Energy Dynamics: Overview

- Crude Oil: International Overview

- Crude Oil: Western Canada

- Crude Oil: Ontario and Eastern Canada

- Natural Gas Liquids

- Natural Gas: Western Canada

- Natural Gas: Ontario and Québec

- Liquefied Natural Gas: Canada’s Role in Global LNG

- Small-Scale Liquefied Natural Gas: An Emerging Demand Trend

- Electricity: Power from Water and Wind

- Electricity: Thermal Generation

- Energy in Atlantic Canada: Natural Gas and Power Markets

- Energy in the North

- Appendix A.1: List of Acronyms

- Appendix A.2: Data Sources

- Appendix A.3: About this Report

- Endnote

Canadian Energy Dynamics: Overview

The energy sector in Canada is continually being shaped by new sources of supply, changing demand, and integrated infrastructure development. The National Energy Board (NEB or Board) believes that well-functioning, competitive markets efficiently balance supply and demand, and lead to innovative and robust energy systems.

In support of its regulatory role, the Board actively monitors energy markets and produces independent, fact-based energy information for Canadians. These products increase the transparency of Canadian energy markets and support Canadian energy literacy. This report, Canadian Energy Dynamics: Review of 2014, describes many important developments witnessed in Canadian energy markets in 2014, while providing useful information and statistics.[1]

Canadian crude oil production has been resilient in the face of constrained pipeline capacity, increased U.S. supply, and falling global oil prices. Greater access to coastal markets, via railroads and from pipeline additions in the U.S., led to the narrowing of oil price discounts in 2014, and higher revenues for Canadian producers. Other factors that assisted earnings for producers include the depreciation of the Canadian dollar and the lower cost of diluent. Pipeline oil exports increased to new highs, in part due to extra capacity leading to higher exports on the Enbridge Mainline system. Crude exports by rail continued a steep increase, reaching over 180 Mb/d by year end. Refineries in Eastern Canada received greater amounts of crude by rail, sourced from Western Canada and the U.S. The rail shipments to the Canadian and U.S. East Coast displaced imports from other countries, while some oil produced from offshore Atlantic Canada has been rerouted to Europe or South America.

Strong production growth in the eastern U.S. from the Marcellus and Utica Shales continue to change gas flows across North America, and notably into Ontario and Québec. In the west, the Montney Formation, which contains roughly 140 times Canada’s annual natural gas needs, continued to produce more gas. There were also numerous successful production tests from the emerging Duvernay Shale in 2014. The Board continued to receive licence applications to export natural gas in liquefied form, primarily to markets in Asia and Europe. Companies have also found new uses for liquefied natural gas, including as an alternative to diesel as a transportation fuel and for power generation.

The development of shale gas has also increased the availability of natural gas liquids, with U.S. propane production growing to new records. This helped drive propane inventories in Canada and the U.S. to record highs after the price spikes and delivery challenges experienced during the Polar Vortex last winter. Also in 2014, the Board received its first licence application for the export of propane to the Asia-Pacific market via the U.S.

The closure of the Thunder Bay Generating Station (photo at left) in April 2014 marked the completion of Ontario’s coal phase out. The plant will be converted to burn biomass starting in 2015. Another milestone was reached when SaskPower completed the carbon capture project at the Boundary Dam coal plant. Across the country, hydroelectric and wind projects were advanced, with construction starting at Muskrat Falls in Newfoundland and approval granted for Site C in B.C.

Crude Oil: International Overview

Prices Decline on Strong U.S. Production and OPEC Maintaining Production Targets

In June, West Texas Intermediate (WTI) and Brent were trading at US$105.23 and US$111.65 per barrel respectively. The ensuing months would see world oil prices fall to the lowest levels since the 2009 recession. This time, however, the fall was not a result of a global economic slowdown. Instead, the rapid expansion in North American oil supply has led to a surplus supply situation. In late November, amid speculation that the Organization of Petroleum Exporting Countries (OPEC) might cut production to support oil prices that had fallen for five consecutive months, OPEC announced it would maintain its crude oil production target of 30 MMb/d. This decision signaled the loss of a key price support mechanism. West Texas Intermediate (WTI) stood at US$73.70 per barrel on November 26, the day before the OPEC meeting, and it fell over 30 per cent to under US$50 per barrel in January 2015. The volume of WTI trading on NYMEX typically bottoms in December; however, in 2014 it increased by 15 per cent – the first increase from November to December since 2009.

The U.S. Energy Information Agency (EIA) estimated that combined U.S. and Canadian oil supply increased by nine, ten and eleven per cent in 2012, 2013 and 2014, respectively. As shown in Figure 1, this continuous growth has exceeded the decline in supply from other non-OPEC nations and the growth in global petroleum demand. Thus, the share of the world market available for OPEC producers has declined. In 2013, OPEC supply was reduced by over one MMb/d, primarily due to geo-political related outages in Libya, Nigeria, Iran and Iraq. Supply from OPEC nations was relatively flat in 2014.

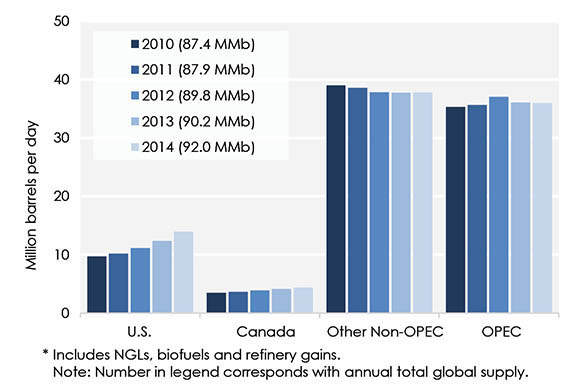

Figure 1 Global Oil and Liquids Supply[*]

Text version of this graph

Source: EIA

Description: This graph illustrates global oil and liquids supply in the U.S., Canada, Other Non-OPEC and OPEC nations from 2010 to 2014. Between 2010 and 2014, global crude oil and liquids production increased from 87.4 million barrels per day to 92.0 million barrels per day, with U.S. supply growing the most.

[*] Includes NGLs, biofuels and refinery gains.

Note: Number in legend corresponds with annual total global supply.

Canadian Crude Oil Searching for New Markets Overseas

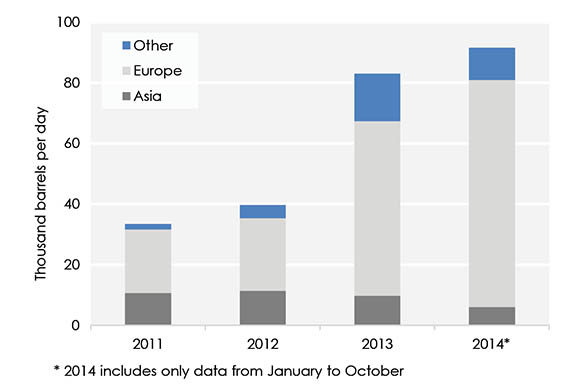

Prior to 2013, Canadian crude oil exports to destinations other than the U.S. were relatively minor, and predominately either light crude shipments from offshore Newfoundland and Labrador to Europe, or Alberta crude shipped from Trans Mountain’s Burnaby, B.C. marine terminal to Asia. However, in the past two years, volumes from Atlantic Canada that historically would have been sent to refineries in Eastern Canada and the U.S. have been sent elsewhere, displaced by growing U.S. supply. Canadian crude exports to Europe have grown to account for over three per cent of total exports, and exports to South America have also increased considerably. Figure 2 shows the breakdown of Canadian crude oil exports to markets other than the U.S.

Figure 2 Crude Oil Exports from Canada to Non-U.S. Destinations[*]

Text version of this graph

Source: NEB

Description: This graph illustrates crude oil exports from Canada to non-U.S. destinations. It shows that exports to non-U.S. countries have grown from 33.4 thousand barrels per day in 2011 to an estimated 91.5 thousand barrels per day in 2014. Exports to Europe account for the vast majority of Canadian crude oil exports to non-U.S. markets.

[*] 2014 includes only data from January to October

In September 2014, Suncor loaded its first tanker of heavy crude on the Canadian East Coast. Western Canadian heavy crude was railed from Alberta to a port near Montreal where it was loaded on a tanker and delivered to Italy. Canadian crudes have also been shipped from American ports to markets in countries such as Spain and Switzerland.

The long term viability of Europe as a market for Canada’s crude oil will depend on, among other things, the price discounts for Canadian crude, security of Russian oil supplies to European refineries and policies that influence the types of crude that are refined in Europe. In October 2014, the European Union proposed amendments to its Fuel Quality Directive that would remove discriminatory treatment of oil sands crude and products. A ratification vote for the directive, as written, will be held in early 2015.

Crude Oil: Western Canada

Higher Western Crude Oil Production and Exports

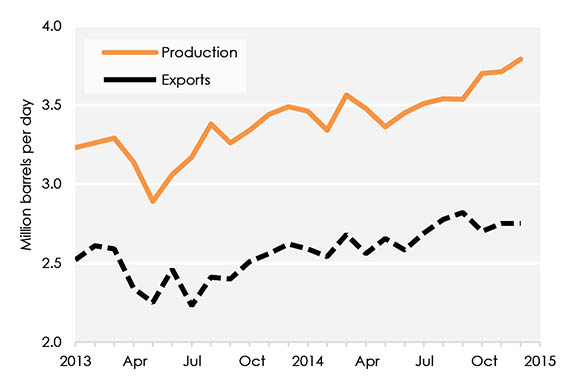

Crude oil production from the Western Canada Sedimentary Basin (WCSB) continued to show significant growth in 2014. Average production was approximately 3.55 MMb/d, representing an 9.2 per cent increase over the previous year, and ended the year at 3.79 MMb/d. Light crude oil production grew by 7.0 per cent as horizontal drilling and multi-stage fracturing techniques were applied in tight oil formations in Alberta (Cardium and Montney) and Saskatchewan (Viking). This continued to reverse a decades-long trend of production decline for light crude oil.

Figure 3 Western Canadian Production and Exports

Text version of this graph

Source: NEB

Description: This graph illustrates Western Canadian monthly crude oil production and exports. Production has increased from 3.23 million barrels per day in January 2013 to an estimated 3.79 million barrels per day in December 2014. Exports have grown slightly, from 2.52 million barrels per day in January 2013 to an estimated 2.72 million barrels per day in December 2014.

In the oil sands, growth from in-situ projects continued to exceed mining projects, a trend that is expected to continue in the future as additional steam-assisted gravity drainage (SAGD) projects start commercial operations. SAGD production averaged 728 Mb/d, which was 25 per cent higher than 2013. Total oil sands production was approximately 2.30 MMb/d, a 10.2 per cent increase over the previous year.

Crude oil exports from Western Canada averaged approximately 2.66 MMb/d in 2014, 8.5 per cent higher than the previous year. Additional capacity on Enbridge’s Canadian and U.S. systems allowed more Western Canadian crude to access markets at lower cost. As a result, crude-by-rail exports did not increase as much as in the previous year. Pipeline exports averaged 2.45 MMb/d with an average price of $91.06 per barrel, whereas total crude-by-rail exports averaged 169 Mb/d with an average price of $88.80 per barrel. In addition, surging domestic production in the United States began to displace Canadian crude-by-rail volumes, primarily in California. However, Western Canadian exports of heavy crude via rail to the U.S. East and Gulf Coast continue showing an upward trend.

Bitumen Prices Slower to Fall than World Benchmarks

Canadian crude oil prices increased at the beginning of the year, peaked during the summer due to favorable market access conditions and record demand in major U.S. refinery markets, then decreased as global crude oil benchmark prices collapsed. Strong U.S. demand for heavier crudes and greater export capacity translated into lower price discounts between Canadian and U.S. crude oil varieties. In addition, a depreciating Canadian dollar lowered the overall impact of falling crude oil prices on Canadian crude producers whose products are sold in U.S. dollars while costs are primarily based in Canadian dollars. Heavy crude oil price discounts, which peaked in early 2013, decreased consistently as the year progressed and are expected to remain at current low levels until production growth surpasses existing transportation capacity.

Statistics from the Alberta Government show that the average value of bitumen at Hardisty, Alberta increased by approximately 17 per cent in 2014 relative to 2013, even after accounting for the price fall that occurred during the second half of the year. In addition to benefiting from lower price discounts and a lower Canadian dollar, the value of bitumen also improved due to lower diluent prices. The Cochin Pipeline, which was reversed in mid-2014, now delivers supplies of condensate (a type of diluent) from the U.S. to Alberta’s market. Diluent is blended with heavy crudes and bitumen to assist in moving it through pipelines.

Overall increases in prices and production translated into higher revenues for the upstream oil sector in Canada. Revenues for this sector increased by 14 per cent relative to 2013 and reached approximately $115 billion which was three-and-a half times the total revenue of the natural gas upstream sector.

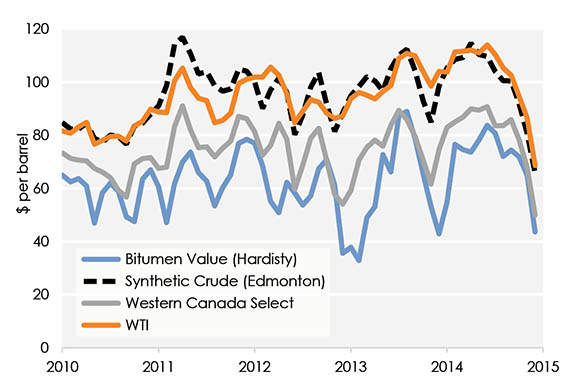

Figure 4 Crude Oil and Bitumen Prices

Text version of this graph

Source: PIRA, the Government of Alberta, and NEB calculations

Description: This graph shows the historical price of three benchmark crudes and bitumen from 2010 to 2014. WTI and synthetic crude at Edmonton have fluctuated around $100 per barrel from 2011 to mid-2014 when crude prices began six months of declines to end 2014 at their lowest prices since 2009. WTI and synthetic crude ended 2014 at $69 and $66 per barrel respectively. Heavier crude benchmarks, such as Western Canada Select traded around $75 per barrel over the period 2001 to mid-2014, while bitumen traded around $65 per barrel. Western Canada Select and bitumen ended 2014 at $50 and $44 per barrel respectively.

Crude Oil: Ontario and Eastern Canada

Declining Crude Imports in Eastern Canada

Crude oil imports into Canada for the first ten months of 2014 averaged 615 Mb/d, 11.2 per cent lower than over the same period in 2013. The downward trend that started in 2008 (Figure 5) is partly related to closures of refineries in Montreal (Shell in 2010), Dartmouth (Imperial in 2013) and most recently, Sarnia (NOVA in June 2014). In addition, refinery demand data from Statistics Canada shows that domestic crude oil has also increased its share of the Canadian refinery market and in particular in Eastern Canada, which receives almost all of the imports. Crude oil imports from offshore regions into Ontario have all but disappeared starting mid-2014.

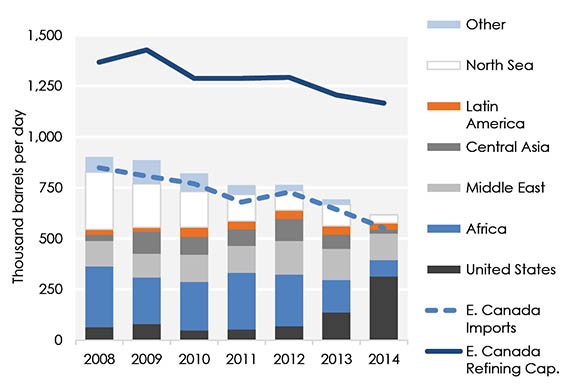

Figure 5 Canadian Crude Oil Imports by Source and Eastern Canada’s Share

Text version of this graph

Source: Statistics Canada

Description: This graph shows Canadian crude oil imports by source, Eastern Canada’s share of these imports, and total refining capacity in Eastern Canada. From 2008 to 2014, imports have decreased from 900 thousand barrels per day to 616 thousand barrels per day. Imports from the North Sea and Africa have declined considerably over this period, and, despite declining total imports, U.S. imports have increased significantly. From 2008 to 2014, U.S. imports increased from 63 thousand barrels per day to 312 thousand barrels per day. U.S. imports now account for more than half of Canadian imports.

Also between 2008 and 2014, refining capacity in Eastern Canada declined from 1.37 million barrels per day to 1.17 million barrels per day.

While total imports have declined, imports from the U.S. have grown from 19.5 per cent of total 2013 imports to 50.7 per cent in 2014, largely at the expense of light oil imports from the North Sea and Africa. Most of the increase is related to growing volumes of Bakken crude oil moved by rail to refineries in Québec and the Maritimes and more recently, Eagle Ford crude moved by tanker from the U.S. Gulf. These lower-priced supplies of light crude oil have been displacing crude oil supplies from offshore Atlantic Canada and offshore imports into Eastern Canada’s refineries. Most of the displaced Atlantic crude oil has been shipped to Europe.

Harvest Operations Corp, the Canadian subsidiary of the Korean National Oil Corp. completed the sale of the Come-by-Chance refinery in Newfoundland to Silver Range Financial Partners LLC of New York on November 17, 2014. The refinery has been struggling with poor margins for years, as it relies on expensive offshore crude oil imports. The new owners plan to continue to operate the refinery, switching it to use U.S. shale oil as feedstock. There was market speculation that the facility would have shut down indefinitely after its September 2014 scheduled maintenance shutdown if no new buyer was found.

Atlantic Offshore Developments Show Potential

Atlantic Canada produces 230 Mb/d annually, about seven per cent of Canada’s total crude oil production, from developments in the Jeanne D’Arc Basin offshore Newfoundland. Projects to develop neighbouring (satellite) fields are underway to extend the life of the existing developments.

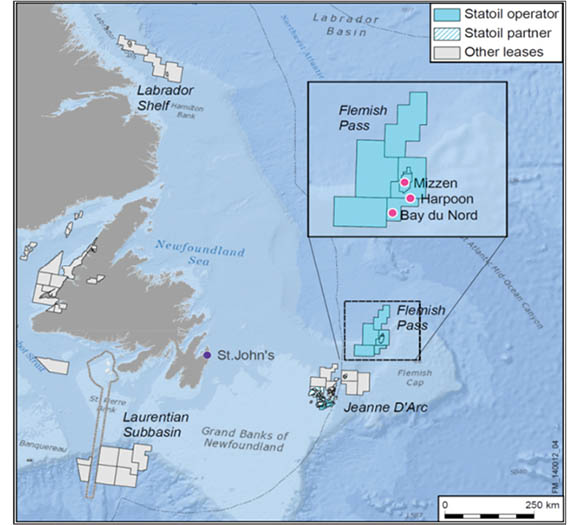

As shown in Figure 6, new discoveries have been made further offshore in the Flemish Pass Basin, but development may be many years into the future. Statoil’s Bay du Nord prospect there was reported to hold up to 600 MMb of recoverable oil and followed two earlier discoveries in the area: Mizzen (estimated at 100 to 200 MMb) and Harpoon.

Figure 6 Exploration in the Flemish Pass Basin

Text version of this map

Source: This map is courtesy of StatOil.

Description: This map illustrates offshore oil exploration in the Flemish Pass Basin, located due east from Newfoundland and on the Flemish Cap of the continental shelf.

In 2011 and 2012, Nova Scotia issued 12 exploration licences for the Nova Scotia Offshore region with a total work expenditure commitment of nearly $2.1 billion. In 2014, Shell and BP conducted seismic and seabed surveying in preparation for drilling, which is anticipated to occur in the 2015 to 2017 time frame.

In November 2014, Junex announced an oil discovery near Gaspé, Québec. This is the first horizontal oil exploration well ever drilled in Québec. Additional exploration wells are planned for 2015.

Natural Gas Liquids

Propane Markets Stabilize After Polar Vortex, Prices Dive in December

The Polar Vortex resulted in near-record cold temperatures across most of Canada and the U.S. during the 2013/14 winter. Wholesale and retail propane prices spiked in response to strong demand and the logistical challenges of delivering propane to end users during extreme weather conditions. To examine these issues faced by propane markets and to investigate the possibility of anti-competitive behaviour by propane firms, the Competition Bureau and NEB released the Propane Market Review in April 2014.

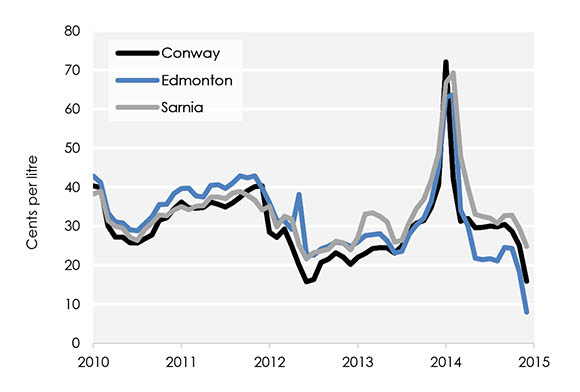

Figure 7 Monthly Average Propane Prices at Major Hubs

Text version of this graph

Source: Butane-Propane News, Bank of Canada, NEB calculations

Description: This graph illustrates monthly average wholesale propane prices at three major North American hubs: Sarnia, Ontario; Edmonton, Alberta; and Conway, Kansas. The graph shows the sharp rise in propane prices at these hubs in early 2014, and the rapid decline that followed.

Since the peak of the propane crisis in January and February 2014, propane prices returned to more normal, seasonal levels for most of 2014 before declining rapidly later in the year. Wholesale prices at Edmonton and Sarnia have declined from highs of 63 and 72 cents/L reached in January 2014 to 8 and 25 cents/L, respectively, in December 2014, primarily due to a very well supplied propane market. While this has resulted in lower prices for propane consumers, it has had a significant negative effect on the fractionation spread (the margin received by midstream companies for extracting liquids from the natural gas stream). Figure 8 illustrates the sharp decline in the spread starting in October 2015.

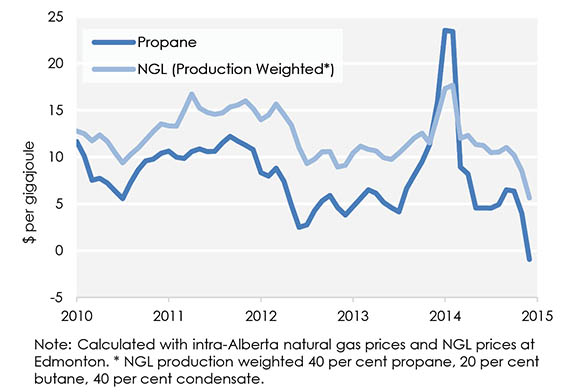

Figure 8 Fractionation Spreads in Alberta[*]

Text version of this graph

Source: NEB

Description: This graph illustrates monthly average fractionation spreads in Alberta for propane and for a production-weighted NGL mix. The fractionation spread is the margin received by midstream companies for extracting liquids from the natural gas stream and in this graph is measured in Canadian dollars per gigajoule. Alongside the sharp increase in prices that occurred in early 2014, the margin earned for extracting liquids increased as well. However, with declining prices for propane that occurred later in 2014, the fractionation spread for propane declined to negative 93 cents per gigajoule. The fractionation spread for NGL mix declined to $5.63 per gigajoule.

Note: Calculated with intra-Alberta natural gas prices and NGL prices at Edmonton.

[*] NGL production weighted 40 per cent propane, 20 per cent butane, 40 per cent condensate.

While the U.S. continues exporting record volumes of propane to overseas markets, the overall supply picture at the beginning of 2015 appears better prepared than it did prior to last winter’s Polar Vortex-driven crisis. U.S. propane production remains robust, with 2014 production approximately 20 per cent higher than 2013 production and now exceeding 1.0 MMb/d. Lastly, propane demand at the start of the 2014 North American crop drying and heating seasons has been lower than 2013, leaving Midwest and Canadian propane storage at high levels. Total underground inventories in Canada and the U.S. on January 1st were 82 per cent higher in 2015 than 2014, sitting at 81.9 million barrels. Inventories in Canada alone on January 1st were at 6.2 million barrels, 134 per cent higher in 2015 than 2014 and 10 per cent higher than the January record previously set in 2002.

The Cochin Pipeline Reverses and Canadian Propane Searches for New Markets

Historically, Canada has produced more propane than it consumes and this surplus production is exported to the U.S. Unlike other hydrocarbons (namely oil and natural gas), Canadian propane is primarily exported by rail. Until March 2014, Western Canada had the option of moving propane to markets in the U.S. Midwest via the Cochin Pipeline. In March, the Cochin Pipeline ceased this service, preparing to reverse direction to import condensate, leaving propane producers more reliant on rail, other pipelines (where propane is mixed with other hydrocarbons, such as Enbridge or Alliance), and to a lesser extent truck, to export propane to the U.S. As a result, midstream firms in Alberta such as Keyera and Plains Midstream are adjusting to the new landscape. Keyera is developing a 40 Mb/d rail terminal in Josephsburg, Alberta while Plains is adding rail capabilities to its Fort Saskatchewan fractionation and storage facility that previously was only served by truck and pipeline.

Some in the propane industry have proposed selling propane to new markets outside of North America. In August 2014, the Board received an application from Pembina for a licence to export propane from Canada for a period of 25 years. Pembina’s 37 Mb/d export terminal would be located in Portland, Oregon but would source propane from Western Canada. Pembina has proposed to begin exporting in 2018. Other firms considering liquids exports from the west coast include AltaGas/Petrogas Energy/Idemitsu Kosan (located in Ferndale, Washington), and Sage Midstream (Longview, Washington).

Natural Gas: Western Canada

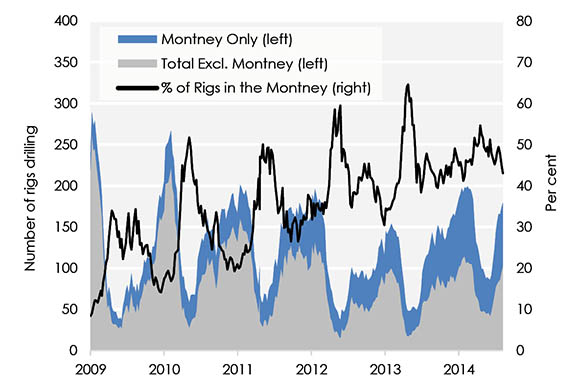

Producers Focusing on Montney Tight Gas

Natural gas production from the WCSB has been relatively stable over the past three years. However, where and how WCSB gas is produced has transformed significantly. Like in the U.S., conventional natural gas drilling has declined dramatically, whereas multi-stage hydraulic fracturing and long-reach horizontal drilling have become the norm. These techniques have focused activity in certain formations in Western Canada, like the Montney.

The Montney Formation straddles the northern part of the Alberta-B.C. border and covers approximately 130,000 square kilometres, roughly the size of Nova Scotia and New Brunswick combined. The Montney primarily produces tight gas (natural gas produced from reservoirs that have significant difficulty producing without being hydraulically fractured). The tight gas resource base of Montney is very large, estimated to contain 449 Tcf of marketable natural gas. To put this in perspective, Canada consumed about 3.2 Tcf of gas in 2013.

Gas drilling activity in the Montney has grown to nearly two-thirds of all gas drilling activity in the WCSB. While other substantial shale and tight gas prospects have been identified in Western Canada such as the Horn River Basin, Liard Basin, Cordova Embayment and Duvernay Shale, the combined number of rigs drilling in those other areas averaged 17 in 2014, compared to an average of 72 rigs operating in the Montney.

Figure 9 Drilling Rigs Inside and Outside the Montney

Text version of this graph

Source: JuneWarren-Nickles

Description: This graph illustrates gas-directed drilling rigs that are in the Montney, and drilling rigs outside of the Montney. While there is heavy seasonality in drilling data, the trend from 2009 shows that the percentage of rigs operating in the Montney has been steadily increasing over time, from around 20 to 30 per cent in 2009 to around 50 per cent in 2014. While the number of gas-directed rigs operating in the Montney has increased from an average 21 in 2009 to an average 70 in 2014.

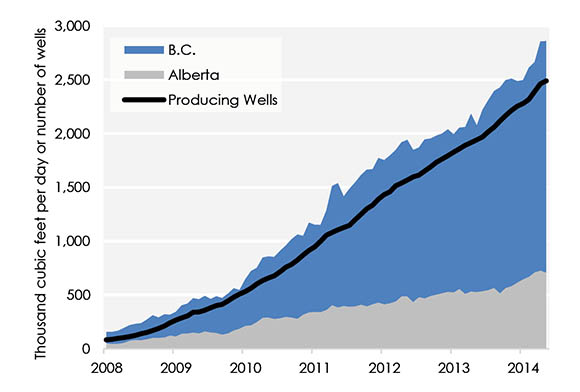

Montney wells are highly productive, with an average production rate of 4.5 MMcf/d during the first three months, over double the 2013 WCSB average rate of 1.9 MMcf/d. Furthermore, significant proportions of natural gas liquids in the gas stream improve the economics of Montney gas. The Montney also benefits from nearby natural gas and NGLs infrastructure, which is there because of previous conventional natural gas activity as well as significant investments already made by the proponents of west coast liquefied natural gas export terminals. For the first half of 2014, total Montney (Alberta and B.C.) marketable production averaged 2.35 Bcf/d, representing 16 per cent of total marketable Canadian gas production, and an increase from the 2013 average of 1.97 Bcf/d.

Figure 10 Montney Natural Gas Production

Text version of this graph

Source: Divestco

Description: This graph illustrates the increases in natural gas production from the Montney in B.C. and Alberta from 2008 to 2014. Production has increased from an average 277 million cubic feet per day in 2008 to an average 3,120 million cubic feet per day in 2014. The number of producing wells in the region has grown ten-fold, from under 250 in 2008 to over 2500 in 2014.

While the Montney is the most active amongst the various gas prospects in Western Canada, other areas still have significant potential. Production tests in the Horn River Basin (estimated to contain 78 Tcf of marketable gas resources) and the Liard Basin have resulted in wells with very high flow rates. Given the right economic conditions, activity in these areas and others outside of the Montney could also contribute to Canadian gas production in the future.

The Uncertain Potential of Duvernay Shale Gas

Production tests in Alberta’s Duvernay basin have demonstrated that its gas has significant amounts of NGLs, which can help the economics of production. While the Duvernay has been labeled a “shale oil” area, most producers have been targeting its rich gas areas (high content of condensate and other NGLs). Duvernay wells have been producing between 100 and 500 barrels of condensate for every million cubic feet of gas – far higher than what is being produced from the Montney and potentially higher than rich gas production from Texas’ Eagle Ford Shale. However, the Duvernay is still in the testing stage of exploration and industry activity. While the Duvernay shows some promise, its wells are expensive and technically challenging and it may take a while before we learn more about its true potential.

Natural Gas: Ontario and Québec

Polar Vortex Shakes Up Ontario and Québec Gas Markets

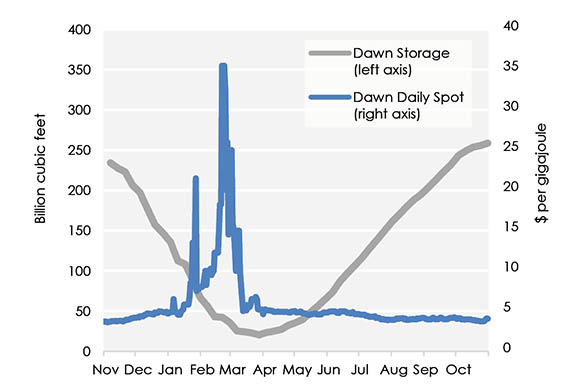

From December 2013 through April 2014 an enduring cold dubbed the Polar Vortex gripped most of Canada and the U.S. and natural gas demand greatly exceeded production. As large volumes of gas in storage were withdrawn, total gas in storage eventually dipped below 25 per cent of storage capacity and prices became volatile. Natural gas prices that were steadily less than $5/GJ increased to over $35/GJ at the Dawn hub in southern Ontario. Figure 11 shows how the natural gas price responded at Dawn to storage levels during the Polar Vortex and later as storage volumes built up in the summer.

Figure 11 Gas Storage in Ontario vs. Dawn Gas Price in 2013/14

Text version of this graph

Source: NGX and Canadian Enerdata

Description: This graph illustrates gas storage volumes in Ontario versus the price of natural gas at the Dawn hub in southern Ontario during the 2013-2014 gas year. The graph shows that as total gas in storage dipped below 50 billion cubic feet, the price of gas at Dawn increased dramatically, reaching a peak price above $35 per gigajoule on February 21, 2014.

Throughout the 2014 summer, analysts were concerned about the market’s ability to refill storage in time for the upcoming 2014-15 winter. However, strong North American production resulted in record injection levels, refilling storage in time for the 2014-15 heating season.

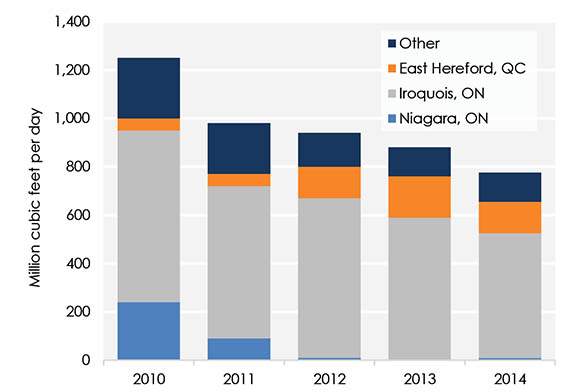

Gas Flows Continue Changing in Ontario and Québec

Historically, Eastern Canada has received most of its natural gas from Western Canada. Natural gas from Western Canada was also exported to the northeast U.S. via several export points in Ontario and Québec. However, the rapid development of the Marcellus Shale in the northeast U.S. is changing this, as gas exports from Ontario and Québec to the U.S. dropped 12 per cent from 2013 to 2014, for a total decline of 38 per cent since 2010 as shown in Figure 12. Some former export points are now being used to both import and export natural gas. In the near future, more export points are expected to be used to import gas from the U.S., either occasionally or permanently.

Figure 12 Exports of Natural Gas from Points in Ontario and Québec

Text version of this graph

Source: NEB

Description: This graph illustrates exports of natural gas from export points in Ontario and Quebec from 2010 to 2014. These exports have been declining steadily, from 1,250 million cubic feet per day in 2010 to 775 million cubic feet per day in 2014. Declines have occurred at all export points except East Hereford.

Pipeline Infrastructure Responds to Changing Gas Flows

Consumers in Ontario and Québec are increasingly aiming to access natural gas from the nearby Marcellus Shale, and several pipeline companies are considering building or expanding pipelines to move natural gas from the U.S. into Ontario and Québec.

Over the last year TransCanada announced plans to invest almost $2 billion to tap into growing Marcellus supplies. TransCanada’s proposed facilities in the “Eastern Triangle” (North Bay-Toronto-Iroquois) include the Eastern Mainline Project, the Parkway West Connection, the Hamilton Area Project, and the Vaughan pipeline project. The proposed King’s North Connection would connect with new Enbridge Gas Distribution pipeline facilities.

Enbridge is proceeding with its Greater Toronto Area Project and is also assessing the feasibility of its proposed Niagara Link Gas Storage that would offer more storage and transportation near the Dawn hub. Spectra Energy and DTE Energy have proposed the NEXUS Gas Transmission Project to further connect Ontario with growing supplies of Marcellus and Utica gas.

Union Gas is also trying to improve access to new, lower cost supplies located in Pennsylvania and Ohio. This includes compressors at Lobo and Parkway West and additional pipeline projects such as the Dawn Parkway System Expansion, Sarnia Expansion, Brantford-Kirkwall Pipeline, and Burlington-Oakville Pipeline.

Liquefied Natural Gas: Canada's Role in Global LNG

Strong Interest in Exporting Canadian Gas as LNG

Global natural gas consumption in 2013 averaged approximately 330 Bcf/d. Of that volume, roughly 32 Bcf/d was transported to market via tankers as liquefied natural gas (LNG). Because natural gas prices in North America are currently lower than global LNG prices, there is significant interest in exporting natural gas from North America in the form of LNG.

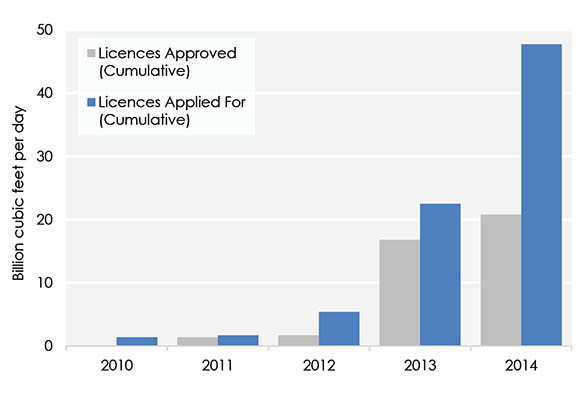

Between 2010 and 2014 the NEB has received over 20 long-term LNG export licence applications. To date, these applications have requested approval for a total of approximately 43 Bcf/d of natural gas for export. While earlier applications specified west coast locations as the export points, more recent applications have proposed export points on Canada’s eastern shores in Nova Scotia and Québec. As of December 2014, the Board had issued 9 LNG export licences for a total of 20.4 Bcf/d. The cumulative volumes of applied for and approved long-term LNG export licences are shown in Figure 13.

Figure 13 Long-Term LNG Export Licence Applications in Canada

Text version of this graph

Source: NEB

Description: This graph shows the quantity of natural gas in billion cubic feet per day contained in all long-term LNG export licence applications in Canada that have been applied for, and approved by the NEB from 2010 to 2014. In 2014, cumulative licence volumes approved totaled 20.8 billion cubic feet per day, while cumulative licence volumes applied for totaled 47.7 billion cubic feet per day.

Canadian Proposals Face Challenges and Global Competition

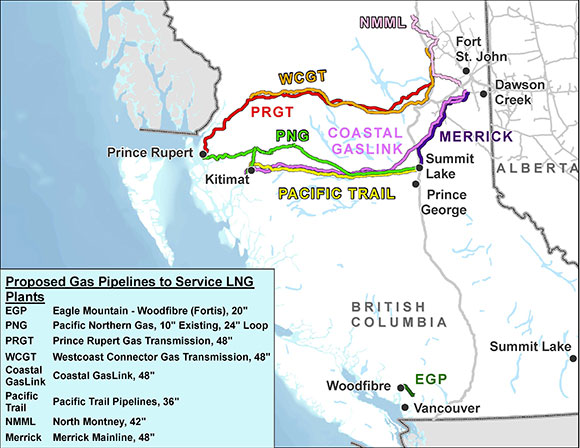

Most LNG liquefaction terminals are multi-billion dollar investments. So far, none of the projects in Canada have broken ground. In December 2014, Petronas announced that it was delaying its final investment decision on the Pacific NorthWest LNG Project due to concerns about project economics. In general, project economics for Canadian LNG projects are affected by factors such as: remote resource locations, remote plant sites, significant environmental and regulatory requirements, and cost considerations. These liquefaction terminals must be constructed from scratch and hundreds of kilometers of pipelines must be built or expanded to transport natural gas from northeast B.C. to the coast. Applications or project descriptions for several LNG-related pipelines in Western Canada have been filed with the B.C. Environmental Assessment Office or the NEB. These pipeline proposals in B.C. are shown in Figure 14. In the Maritimes, the existing Maritimes & Northeast Pipeline would likely need to be expanded to accommodate higher volumes of gas flowing north to Canada for export as LNG.

Figure 14 Proposed Pipeline Projects for West Coast LNG Facilities

Text version of this map

Source: NEB

Description: This map illustrates the various pipelines that have been proposed in British Columbia to deliver natural gas to potential LNG liquefaction facilities for export to overseas markets.

Canadian proposals face competition from projects around the globe. In the U.S., over 40 export applications have been filed requesting a total volume of almost 50 Bcf/d of LNG exports. A number of the facilities proposed in the U.S. consist of converting existing underutilized LNG import terminals into export terminals and would cost less than proposed Canadian greenfield projects. There are currently four liquefaction facilities under construction in Louisiana, Texas and Maryland. In other parts of the world, liquefaction terminals are under construction or have been proposed in Australia, Russia, Mozambique, Nigeria and other countries.

Although global demand is expected to grow at over three per cent per year, the volume of proposed LNG exports from North America alone exceeds projected world demand growth over the next 20 years. This suggests only the most competitive projects will proceed. Finally, LNG contracts are typically indexed to crude oil prices, so any sustained decline in crude oil prices will likely dampen investment in new LNG liquefaction terminals.

Small-Scale Liquefied Natural Gas: An Emerging Demand Trend

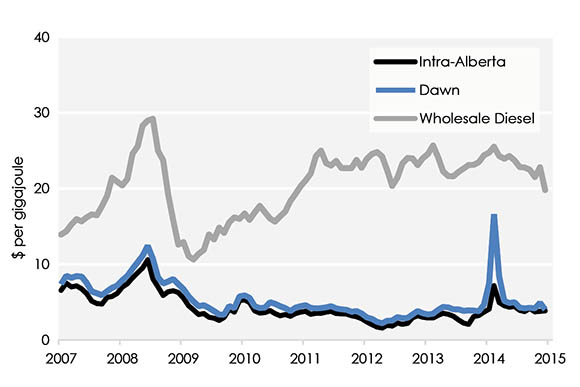

To date, the adoption of LNG as an alternative to diesel has mainly been impeded by the lack of refueling and liquefaction infrastructure. In 2014, there were signs that this issue is being addressed. It appears that, even with recently lower crude oil and diesel prices, LNG remains an economic alternative to diesel for transportation and electric generation. As an example, ENN Canada is currently charging $0.81 per diesel litre equivalent (after taxes) of LNG at its station in Merritt, B.C. In the nearby city of Kamloops, B.C., the wholesale diesel price was comparable at $0.65/L in December 2014, while the retail price was significantly higher, at $1.20/L.

Table 1 Existing and Proposed Small-Scale LNG Facilities in Canada

| Company | Facility Location | Date Commissioned /Expected |

Expansion Date | Capacity (MMcf/d) | |

|---|---|---|---|---|---|

| Current/ Proposed |

Expansion/ Potential |

||||

Source: Various sources [*] Represents Altagas’ planned small-scale LNG expansion across B.C. and not necessarily at the Dawson Creek facility. [**] Currently only available for Union North system integrity requirements. |

|||||

| AltaGas | Dawson Creek, BC | 2015 | By 2020 | 1.65 | 41.30[*] |

| Encana | Strathmore, AB | 2013 | - | 0.41 | - |

| FerusNGF | Vancouver, BC | 2016 | - | 8.26 | - |

| FerusNGF | Edmonton, AB | 2016 | - | 8.26 | - |

| FerusNGF | Elmworth, AB | 2014 | N/A | 4.13 | 20.65 |

| FortisBC | Tilbury Island, BC | 1971 | 2016 | 4.24 | 36.74 |

| FortisBC | Mt. Hayes, BC | 2011 | - | 7.50 | - |

| Gaz Métro | Montreal, QC | 1969 | 2016 | 10.04 | 29.22 |

| Northeast Midstream |

Thorold, ON | 2016 | - | 29.74 | - |

| Stolt LNGaz | Bécancour, QC | 2018 | - | 70.33 | - |

| Union Gas | Hagar, ON | 1968 | 2015 | N/A[**] | 3.00 |

Midstream Infrastructure Developments

In May 2014, Ferus Natural Gas Fuels (Ferus NGF) opened a small-scale liquefaction facility in Elmworth, Alberta, while Altagas Ltd plans to build a facility in Dawson Creek, B.C. Furthermore, several LNG facilities used for peak-shaving (that is, balancing loads or providing temporary storage during peak demand periods) are looking at expanding capacity to accommodate increased demand for LNG. FortisBC announced the expansion of its Tilbury Island, B.C. liquefaction facility, while Gaz Métro plans to triple the output from its Montreal LNG and storage facility. In Ontario, Union Gas filed with the Ontario Energy Board to begin selling LNG from its Hagar LNG facility to interested parties in the region. Stolt LNGaz is proposing to build a new facility in Bécancour, Québec to serve remote communities via tanker trucks, and Northeast Midstream is proposing to build a facility in Thorold, Ontario to potentially serve emerging LNG markets in the U.S.

Along several of Canada’s main freight corridors, natural gas refueling infrastructure for heavy duty freight vehicles continues to grow with the hopes of displacing higher cost diesel fuel. Shell’s refueling station in Calgary is fueled by Encana’s liquefaction facility in Stathmore, Alberta and ENN Canada is proposing to open new facilities in Edmonton and Vancouver to coincide with Ferus NGF’s planned facilities. ENN Canada also has one LNG refueling station along the Highway 401 corridor in Woodstock, Ontario and two along B.C.’s trucking routes in Chilliwack and Merritt. Gaz Métro is developing its “Blue Road” project linking Toronto and Quebec City and currently has three public LNG refueling sites running in Cornwall, Ontario, and, Levis and Sainte-Julie in Québec.

Figure 15 Wholesale Natural Gas and Canadian-Average Diesel Prices

Text version of this graph

Source: Canadian Natural Gas Focus (GLJ), Bank of Canada, and Natural Resources Canada

Description: This graph illustrates natural gas in Alberta and at Dawn, and Canadian-average diesel prices in Canadian dollars per gigajoule. As shown, the price of wholesale diesel (minus taxes, transportation costs and retail mark-ups), is considerably higher than the price of natural gas on an energy unit basis.

New Demand for Canadian Natural Gas Starting to Materialize

Development of small-scale LNG infrastructure have also helped in facilitating a diverse variety of end-user interest in Canadian LNG. BC Ferries plans to have five vessels using dual diesel/LNG-fuelled engines by 2018 and Sociétés des Traversiers du Québec will begin commissioning three similar ferries in 2015. In Québec, Group Desgagnés ordered two freight vessels and Seaspan Ferries Corporation ordered two ferries, both for delivery in 2016. In Alberta, Shell and Caterpillar have agreed to test LNG on heavy-haulers in the oil sands starting in 2016, while CN is testing it as a locomotive fuel. In the oil and gas services sector, Prometheus Energy has imported LNG via truck, and Ferus opened its Elmworth facility in the heart of the Montney tight gas region.

LNG is emerging as an alternative to diesel fuel in areas that lack or have constrained natural gas distribution. A power plant in Inuvik has converted to LNG, and Yukon Energy has been approved to start trucking LNG to Whitehorse. While Gaz Métro sold LNG to power plants in New England in 2014, the company also plans to truck LNG to remote communities and industries in Québec. Perhaps the most exotic new use for Canadian LNG is in Hawaii, where Hawaiian Electric has committed to purchasing LNG from the Tilbury Island LNG expansion for 15 years starting in 2017.

Electricity: Power from Water and Wind

Canadian Hydro Developments Move Ahead

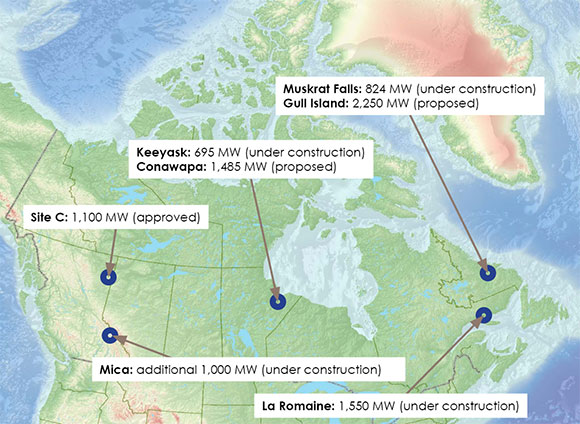

Hydroelectricity constitutes 59 per cent of the 127,762 MW of installed generating capacity in Canada. New projects and upgrades to existing dams currently under construction and slated to become operational between 2014 and 2020 will add 4,569 MW of capacity. Construction is underway on the La Romaine project in Québec, the Muskrat Falls project in Labrador and the Keeyask dam in Manitoba. Keeyask received approval from the Manitoba government in mid-2014.

In B.C., new hydro electric projects and upgrades are planned to meet the expected 40 per cent increase in electricity demand over the next 20 years. The installation of a fifth and sixth turbine at the Mica dam in 2015 will add 1,000 MW of capacity. In December, the provincial government approved the 1,100 MW Site C project to be located on the Peace River in northeastern B.C. Construction on the $8.8 billion facility is expected to start in summer 2015 although the project faces opposition and potential legal challenges.

Historically, the provinces with the most hydroelectric capacity have led the country in electricity exports. However, plans to build hydro-electric dams specifically to service export markets have stalled in recent years as electricity prices in the U.S. dropped on lower demand and lower natural gas prices.

On the other hand, environmental regulations and the retirement of coal-fired generating plants in the U.S. open new opportunities for hydro-electric exports from Canada. In Manitoba, work proceeds on the Manitoba-Minnesota Transmission Project which is needed to service new sales agreements between Manitoba Hydro and U.S. utilities. New power lines to the U.S. have also been proposed in Québec and Ontario.

Figure 16 Map of Canadian Hydroelectric Projects with Capacity and Status

Text version of this map

Source: NEB

Description: This map illustrates hydroelectric facilities in Canada that are proposed, approved or under construction. In B.C., Mica is under construction and Site C has received approvals from the B.C. government. In Manitoba, Keeyask is under construction while Conawapa is proposed. In Quebec, La Romaine is under construction. In Labrador, Muskrat Falls is under construction and Gull Island is proposed.

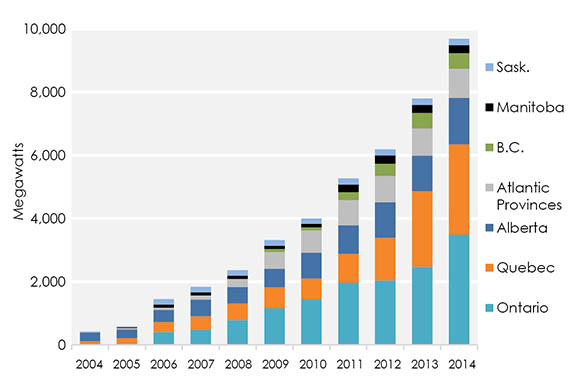

Strong Growth Continues for Wind Energy

As shown in Figure 17, over 1,400 MW of wind capacity was installed in Canada in 2014, somewhat below the 1,600 MW added in 2013. Most of the new projects were located in Québec, Ontario and Alberta. These are the three largest electricity markets in the country and these markets all offer unique advantages for wind developers. Industries in Alberta have used credits gained from wind generation against emissions charges under provincial regulations which were extended from expiry in December 2014 to at least June 2015. In Québec, vast hydroelectric supplies can be used to back-up wind power. Lastly, in Ontario, the stable investment environment created by Ontario’s Feed-In-Tariff program has led not only to it leading Canada in wind power capacity, but has also helped reduce the cost of other renewable technologies such as solar photovoltaic cells.

Figure 17 A Decade of Growth for Installed Wind Capacity

Text version of this graph

Source: Canadian Wind Energy Association

Description: This graph illustrates the growth in installed wind energy capacity in Canada from 2004 to 2014. In 2004, only 433 MW of wind capacity was installed in Canada. In 2014, the installed capacity has grown to 9,209 MW – a growth of twentyfold. Ontario, Quebec and Alberta have 80 per cent of total Canadian wind capacity.

Total installed wind capacity in the country grew to 9,219 MW as of December 2014, which represents about seven per cent of total installed capacity. However, electricity production can be uncertain due to fluctuating wind strength. For that reason, the percentage of electricity actually produced from wind tends to be significantly lower than the share of wind in total installed capacity. During the first ten months of 2014, about 1.4 per cent of electricity produced in Canada was generated from wind.

Electricity: Thermal Generation

An Era Ends for Coal, Another Begins

In April 2014, the Thunder Bay Generating Station ended its coal-fired operations, marking the completion of Ontario’s coal plant phase-out. The station will be converted to burn biomass starting in 2015 with an expected capacity of approximately 150 MW. The transition away from coal started in 2005 when Toronto’s Lakeview plant was shut down. As the coal plants were gradually phased-out over the past decade, Ontario pursued replacement supply including contracting for new gas-fired plants, establishing fixed rates to procure renewables, and enhancing the transmission system. Ontario now has more gas-fired generation capacity than hydro-electric capacity, and it has more wind capacity than any other province.

While Ontario has chosen to shut-down all of its coal plants, Saskatchewan has taken a different approach to mitigating the environmental impact of coal-fired generation. In October 2014, the world’s first commercial scale coal plant equipped with carbon capture and storage (CCS) technology was placed into service at Boundary Dam, Saskatchewan. While generating about 110 MW of power onsite, the Boundary Dam CCS facility captures 90 per cent of the carbon dioxide produced from the coal burn and then pipes it into nearby oil reservoirs for enhanced oil recovery.

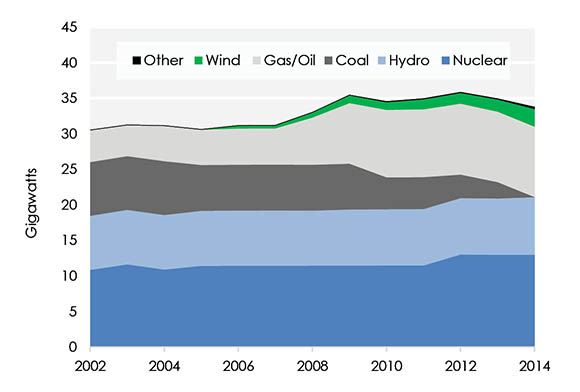

Figure 18 Available Installed Capacity in Ontario

Text version of this graph

Source: IESO

Description: This graph illustrates available installed capacity for electricity generation in Ontario from 2002 to 2014. Nuclear capacity has increased in 2012 with the connection of Bruce Unit 2 to the grid for the first time in 17 years. Hydro capacity has remained relatively steady. Starting in 2009, Ontario’s coal capacity was declining as part of the province’s coal phase-out legislation. New gas-fired generation and renewables (wind and solar) have made up the difference. In 2014, total installed capacity was 33.8 gigawatts.

In Canada, most private sector investors have indicated that the lower cost and shorter timelines for building gas-fired generation make it preferable to building or retrofitting coal plants with CCS units. However, the potential for higher natural gas prices over time, lack of access to gas in certain areas, or evolving GHG regulations could lead to greater consideration of CCS units. In the U.S., there are two major CCS projects scheduled to be completed in 2015 or 2016, and the Global CCS institute has identified twenty other major CCS projects in the power sector worldwide.

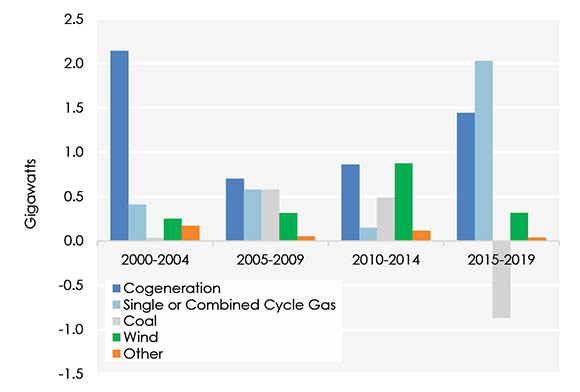

Cogeneration Leads New Capacity Builds in Alberta

New generation added to Alberta’s fleet since the market was deregulated in the late 1990s has been dominated by natural gas-fired units, specifically cogeneration. Three out of the seven generators installed in Alberta in 2014 were small cogeneration units, while two large units at Imperial Oil’s Cold Lake and Kearl oil sands operations were near completion by year-end. Many companies or institutions have chosen to build cogeneration units to supply both power and heat to their facilities. Universities and hospitals can use the steam in district heating systems, whereas the oil sands producers primarily use the steam to heat or upgrade bitumen. Due to unfamiliarity with the power industry, some oil sands companies are reluctant to invest in cogeneration units. However, having power on site has unique benefits, such as reliability of the operation’s power supply, less exposure to the steadily increasing transmission costs in the province, and additional revenue from selling any excess power in Alberta’s market.

Figure 19 Generation Capacity Additions/Retirements in Alberta

Text version of this graph

Source: Alberta Government and AESO

Description: This graph illustrates historical and forecast generation capacity additions and retirements in Alberta. Between 2010 and 2014, the majority of additions in Alberta have been co-generation and wind, followed by coal, single or combined cycle gas, and other. A total of 2.5 gigawatts of capacity was installed during that period. Looking ahead to 2015 to 2019, a total of 3.0 gigawatts of capacity is planned, primarily single or combined cycle gas, followed by co-generation and then wind. A net total of 0.9 gigawatts of coal-fired generation is expected to be retired over this period.

In its most recent long term forecast, the Alberta Electric System Operator (AESO) estimated the cost of building cogeneration for power supply to be higher than combined-cycle units or wind, and similar to that of simple-cycle gas-fired units at around $105-110/MW.h over the life of the project. However, if a reasonable value for the steam production is applied, the estimated cost of the power drops to below any other generation type. The AESO estimates that combined-cycle units will lead all generation additions for the remainder of the decade. However, aside from Calgary’s 800 MW Shepard Energy plant scheduled for completion in 2015, many utilities’ projects appear to be uncertain given the potential for excess electricity supply from new oil sands cogeneration units to lead to lower electricity prices.

Energy in Atlantic Canada: Natural Gas and Power Markets

A Natural Gas Market Tied to New England’s Market

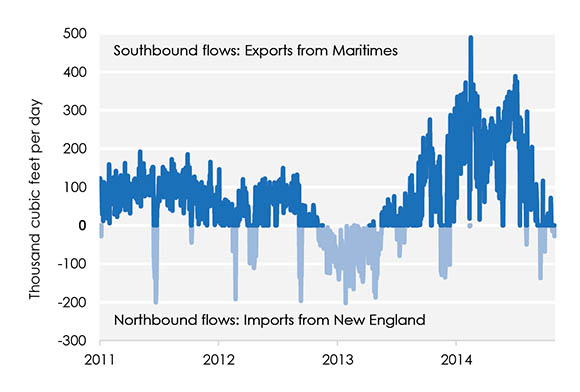

Energy prices in Atlantic Canada are generally higher than in other provinces. For example, higher natural gas prices in the region, particularly during the winter, are due to limited natural gas production in the Maritimes, lack of regional gas storage facilities and ongoing pipeline bottlenecks in the U.S. northeast. There are no trading hubs in the Maritimes, so natural gas is priced based on regional trading hubs such as Dracut or Algonquin, both located in Massachusetts. The winter 2014 spot price for natural gas averaged US$7.98/MMBtu ($8.34/GJ) at Algonquin and US$16.64/MMBtu ($17.39/GJ) at the smaller and less active Dracut hub. For most of 2014, the Maritimes was a net exporter of natural gas. However, on certain days when Atlantic Canada’s offshore production was low, the Maritimes imported natural gas on the bidirectional Maritimes & Northeast Pipeline (M&NP) (see Figure 20).

Figure 20 Daily Flows on the Maritimes & Northeast Pipeline

Text version of this graph

Source: Spectra Energy

Description: This graph illustrates daily gas flows on the bidirectional Maritimes and Northeast Pipeline. On most days in early 2013, the pipeline flowed north. Later in 2013, and utilization of the Maritimes and Northeast Pipeline increased, and gas flowed in a more normal southbound direction.

During January to October 2014, natural gas demand in the Maritimes averaged approximately 175 MMcf/d. Over the same period, production from the two offshore fields in the Maritimes, Sable Island and Deep Panuke, averaged approximately 320 MMcf/d. The Canaport LNG terminal in New Brunswick provided another 50 MMcf/d into the region. Canaport’s output was low, however, because high LNG prices globally discouraged LNG imports into New Brunswick.

While there are plans to expand the capacity of M&NP or improve interconnections with other pipelines, additional pipeline capacity into the region will not be available in the short term. The Maritimes’ first natural gas storage facility started construction in late 2014 and will have an initial capacity of 4.0 Bcf. When commissioned, the storage facility is anticipated to moderate price volatility in the region. Lastly, 2014 saw increasing deliveries of compressed natural gas by truck to customers in the Maritimes and Maine.

Electric Utilities Looking to New Versions of Old Technologies

Power prices have also been of concern in Atlantic Canada. A significant portion of the power price is related to fuel prices, and prices for gas, coal and oil tend to be higher there than other parts of the continent. Over the past decade, Nova Scotia Power has shifted away from heavy fuel oil and has used natural gas instead. However, given the high gas prices in the region and declining oil prices, recent regulatory filings indicate that Nova Scotia Power will reverse this trend by using more heavy fuel oil this winter.

In 2014, construction started on the Muskrat Falls generating station in the Labrador Peninsula’s Lower Churchill area. Construction also began on the associated transmission lines that will bring power to Newfoundland and the Maritimes. The Upper Churchill hydroelectric dam was built in 1970, and Newfoundland and Labrador has now made concrete progress in increasing the region’s power production. The power from Muskrat Falls will allow the province to reduce its use of oil-fired generation.

In October 2014, FORCE, an organization supported by federal and provincial governments and private industry, completed construction of subsea cables in the Bay of Fundy’s Minas Passage. This was an early and significant step in increasing the area’s power from tidal energy. Nova Scotia’s first tidal power plant was built in 1984, adding 20 MW of power to the grid. FORCE’s infrastructure will allow four tidal generators to employ different electric turbine technologies. The potential for tidal energy from the Minas Passage has been estimated at 2,500 MW, with total potential in the Bay of Fundy many times larger.

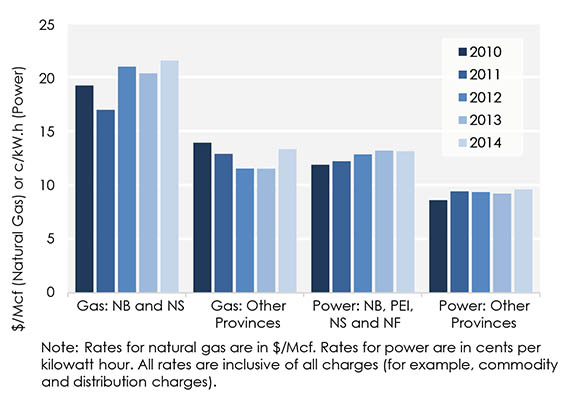

Figure 21 Average Residential Rates for Natural Gas and Power[*]

Text version of this graph

Source: Statistics Canada and Hydro-Québec

Description: This graph illustrates average natural gas and power rates in Atlantic provinces and other provinces from 2010 to 2014. Natural gas and power rates in the Atlantic provinces tend to be higher than in other parts of the country.

[*] Note: Rates for natural gas are in $/Mcf. Rates for power are in cents per kilowatt hour. All rates are inclusive of all charges (for example, commodity and distruibution charges).

Energy in the North

Onshore Oil and Gas Production in the North

The NEB currently has regulatory responsibilities for oil and gas exploration and production activities in Nunavut. In April 2014, regulation of the oil and natural gas industry in the onshore Northwest Territories (N.W.T.) was transferred from the NEB to the Government of the N.W.T. in a process referred to as devolution. In November 2014, the N.W.T. had its first Oil and Gas Call for Nominations for land in the Central Mackenzie Valley and the Mackenzie Delta/Arctic Islands. If any parties expressed interest in acquiring petroleum exploration rights, a call for bids on the nominated lands will be issued in early 2015.

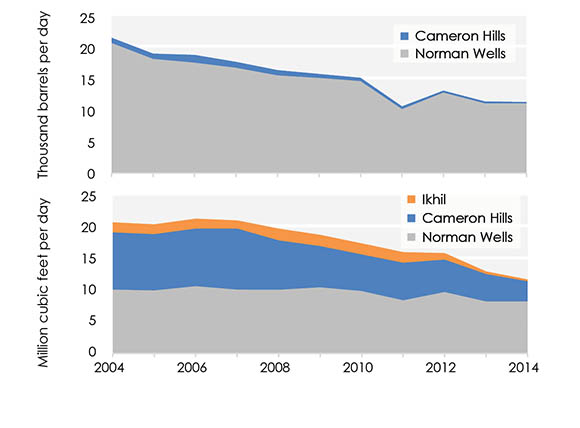

In June the N.W.T. announced that it plans to review the regulations on hydraulic fracturing that it inherited from the NEB and develop its own filing requirements. Such regulations would guide development of crude oil in its Canol shale. As illustrated in Figure 1, N.W.T. oil production declined slightly in 2014, down 0.6 per cent. N.W.T. natural gas production continued a steady decline, down 9.8 per cent for the year.

Figure 22 Oil (Top) and Gas (Bottom) Production in N.W.T.

Text version of this graph

Source: NEB

Description: These two graphs illustrate oil and natural gas production in the Northwest Territories from 2004 to 2014. Over this ten year period, both oil production and natural gas production have declined.

Potential Offshore Drilling in the Beaufort Sea

Imperial Oil Resources Ventures and Chevron Canada Ltd. both requested advanced rulings from the NEB on whether their proposed well control methods would meet the intended outcome of the NEB’s Same Season Relief Well (SSRW) policy. The Board agreed to conduct SSRW technical proceedings. However, in December 2014, Chevron withdrew from the technical proceeding and put its drilling plans on hold indefinitely, citing economic uncertainty in the oil industry.

Electricity Generation Alternatives Growing

While hydro-electricity makes up roughly half of the electricity generated in the North, diesel generation is used to service peak loads and remote areas. The high cost of diesel and delivery via truck makes generation in the North the most costly in Canada. A drought in the summer of 2014 decreased reservoir levels at the Snare Hydro dam and will likely increase the need for diesel generation over a two year span. To prevent the highest power prices in the country from rising further, the N.W.T. government is covering the local utility’s projected $20 million incremental diesel costs over the next two years.

Due in part to these high costs, 2014 saw several signs of the Yukon and the N.W.T. making long-term plans to decrease their reliance on diesel generation. The Yukon Energy Corporation (YEC) has decided to integrate five to ten MW of wind generation into its power plan and is currently deciding between Tehcho or Mount Sumanik for the wind farm’s location. Northwest Territories Power Corporation (NTPC) plans to construct a 54 kilowatt solar and electricity storage pilot project in Colville Lake. NTPC also announced that 2015 will see promotion of a net metering program to encourage renewable usage.

LNG also gained momentum as a power alternative. NTPC has been trucking LNG from Tilbury, B.C. to displace diesel power generation in Inuvik and YEC has received approval to truck LNG into Whitehorse for the same purpose. The success of the Inuvik conversion led NTPC to consider performing similar fuel switches in Yellowknife and Fort Simpson. Both YEC and NTPC have stated that they plan to capitalize on closer liquefaction facilities than Tilbury as they are constructed, which should further reduce the price paid by end-users.

Figure 23 NTPC’s Inuvik LNG Storage Facility

Photo Description

Source: NTPC

Description: NTPC’s LNG storage facility in Inuvik, Northwest Territories

Appendix A.1 List of Acronyms

Photos: Top left: The Town Clock in Halifax lit up on a foggy night.

Right: Warm and rich fall colours on trees in a park.

Bottom left: Power lines against a partially cloudy sky.

Appendix A.2 Data Sources

| Figure/Table | Source |

|---|---|

| Figure 1 | EIA |

| Figure 2 | NEB |

| Figure 3 | NEB |

| Figure 4 | PIRA, Government of Alberta, NEB calculations |

| Figure 5 | Statistics Canada |

| Figure 6 | StatOil |

| Figure 7 | Butane-Propane News, Bank of Canada, NEB calculations |

| Figure 8 | NEB |

| Figure 9 | JuneWarren-Nickles |

| Figure 10 | Divestco |

| Figure 11 | NGX, Canadian Enerdata |

| Figure 12 | NEB |

| Figure 13 | NEB |

| Figure 14 | NEB |

| Table 1 | Various sources |

| Figure 15 | Canadian Natural Gas Focus (GLJ), Bank of Canada, Natural Resources Canada |

| Figure 16 | NEB |

| Figure 17 | Canadian Wind Energy Association |

| Figure 18 | IESO |

| Figure 19 | Alberta Government, AESO |

| Figure 20 | Spectra Energy |

| Figure 21 | Statistics Canada, Hydro-Québec |

| Figure 22 | NEB |

| Figure 23 | NTPC |

A power line pole stands beside an old building in historic Annapolis Royal, Nova Scotia.

A power line pole stands beside an old building in historic Annapolis Royal, Nova Scotia.

Appendix A.3 About this Report

The NEB is an independent federal regulator whose purpose is to promote safety and security, environmental protection and efficient infrastructure and markets in the Canadian public interest within the mandate set by Parliament for the regulation of pipelines, energy development, and trade.

The Board's main responsibilities include regulating:

- the construction, operation and abandonment of oil and gas pipelines that cross international borders or provincial/territorial boundaries, as well as the associated pipeline tolls and tariffs;

- the construction and operation of international power lines, and designated interprovincial power lines; and

- imports of natural gas and exports of crude oil, natural gas, oil, natural gas liquids (NGLs), refined petroleum products and electricity.

Additionally, the Board has regulatory responsibilities for oil and gas exploration and production activities in frontier lands not otherwise regulated under joint federal/provincial accords. These regulatory responsibilities are set out in the Canada Oil and Gas Operations Act, the Canada Petroleum Resources Act (CPR Act).

For oil and natural gas exports, the Board’s role is to evaluate whether the oil and natural gas proposed to be exported is surplus to reasonably foreseeable Canadian requirements, having regard to the trends in the discovery of oil or gas in Canada. The Board monitors energy markets, and assesses Canadian energy requirements and trends in discovery of oil and natural gas to support its responsibilities under Part VI of the National Energy Board Act (the NEB Act). The Board periodically publishes assessments of Canadian energy supply, demand and markets in support of its ongoing market monitoring. These assessments address various aspects of energy markets in Canada. This report, Canadian Energy Dynamics: Review of 2014 is one such assessment that examines elements of Canadian energy markets and how these elements changed in 2014.

If a party wishes to rely on material from this report in any regulatory proceeding before the NEB, it may submit the material, just as it may submit any public document. Under these circumstances, the submitting party in effect adopts the material and that party could be required to answer questions pertaining to the material. This report does not provide an indication about whether any application will be approved or not. The Board will decide on specific applications based on the material in evidence before it at that time.

Photos: Top: Car lights streak by at night in Calgary’s Beltline district.

Bottom left: A rail bridge across the Ottawa River.

Bottom right: The sun sets on a frozen lake in the middle of winter.

Endnote

[1] Some annual statistics quoted in this report include estimates for one or more months of 2014 data.

- Date modified: